How Danish healthcare authorities will create the short list for final software vendor selection

When the Capital Region of Denmark, which includes the municipalities of Copenhagen, Bornholm and Frederiksberg and the Administrative Region of Zealand (RH/RS) make the decision on which of the three suppliers to invite to the final selection process, we foresee that 14 criteria will provide the decision-making basis.

When the Capital Region of Denmark, which includes the municipalities of Copenhagen, Bornholm and Frederiksberg and the Administrative Region of Zealand (RH/RS) make the decision on which of the three suppliers to invite to the final selection process, we foresee that 14 criteria will provide the decision-making basis.

The Capital Region of Denmark and The Administrative Region of Zealand (RH/RS) are in the process of selecting a vendor for their c. DKK 1 billion (€135M) investment in a new IT-healthcare platform.

The purpose of the tender is to ensure that the chosen IT-healthcare platform will meet the defined requirements for IT support of clinical and administrative work within the health care organizations of Zealand. The healthcare platform will need to support close to 40,000 IT users. It will need the capacity to be used by up to 12,000 clinical and administrative users at 17 hospitals and 54 other healthcare institutions simultaneously.

The chosen IT-healthcare platform is expected to start a pilot operation in 2014 in the Capital Region, be commissioned in early 2015 throughout Zealand and then rolled out towards the end of 2016 in the rest of eastern Denmark.

The fourteen criteria for the final selection

Selecting a vendor for such a huge investment is obviously a scary endeavor. Spending €135M of the taxpayers’ money, affecting the daily life of 40,000 well-educated and outspoken employees serving 2.5 million people will thrust the decision-makers firmly into the spotlight.

Selecting a vendor for such a huge investment is obviously a scary endeavor. Spending €135M of the taxpayers’ money, affecting the daily life of 40,000 well-educated and outspoken employees serving 2.5 million people will thrust the decision-makers firmly into the spotlight.

How do you select the best system/vendor and how do you justify the selection?

We have anticipated the main decision-making criteria.

Here they are:

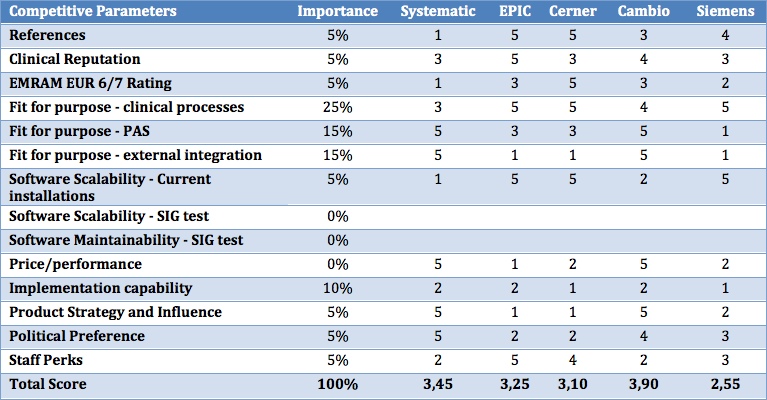

- Installed base and references

- Clinical reputation

- HIMSS/EMRAM level 6/7 certifications (Electronic Medical Record Adoption Model)

- Fit for purpose – clinical processes

- Fit for purpose – PAS

- Fit for purpose – external integration

- Software scalability – current installed base

- Software scalability (SIG test)

- Software maintainability (SIG test)

- Price/Performance

- Implementation capability

- Product strategy and influence

- Political preference

- Staff perks and community participation

The current vendor rating

This is our assessment of the current ranking of the five prequalified vendors after the first round, but before the proposals have been submitted:

- Cambio (with Netcompany) takes the first position

- Systematic (fronted by IBM) comes second

- EPIC (with NNIT) comes third

- Cerner (with CGI, previously Logica) comes fourth

- Siemens (with KMD and ATOS) comes fifth

The rating is obviously a snapshot based on how we see the current (mid February 2013) importance of each criterion. The rating as well as the importance will change as the project progresses and the priorities change. Please see the notes at the end of this post.

Vendor responses

Each vendor received their individual rating and assessment for commenting on Wednesday, February 6th, 2013.

- Systematic responded, but did not wish to make any comments to their rating and assessment.

- Epic, Cambio and Cerner returned elaborate responses. We have included the factual corrections they provided and have included their comments where they apply. We have also changed our rating where justified by the information provided. Thank you very much for participating!

- Siemens didn’t respond.

Let’s take a look at the vendors one by one:

![]() Epic is the Rolls Royce of IT healthcare platforms. The company has been around for more than 30 years. They became “world famous” in 2003 when Kaiser Permanente, which is one of (if not the) most modern and effectively driven healthcare plans in the world, chose EPIC over IBM and Cerner. EPIC has a turnover of approx. $1.5B, employs more than 6,300 people and has made some international traction.

Epic is the Rolls Royce of IT healthcare platforms. The company has been around for more than 30 years. They became “world famous” in 2003 when Kaiser Permanente, which is one of (if not the) most modern and effectively driven healthcare plans in the world, chose EPIC over IBM and Cerner. EPIC has a turnover of approx. $1.5B, employs more than 6,300 people and has made some international traction.

References

Epic has 285 customers and Epic systems will handle more than 100 million patients when all their current customer projects are fully implemented. Epic is a top performer on references. We give Epic the highest score of 5.

Clinical reputation

Although the company operates very much under the radar and is still privately held, there is hardly anyone in the healthcare industry that is not familiar with Epic. They have an excellent reputation in the healthcare industry and are represented at all major international events. Highest score of 5.

HIMSS/EMRAM level 6/7

Had we been in the USA, Epic would also have received a top score in HIMSS/EMRAM level 6/7 installations. Epic has three Stage Six HIMSS/EMRAM hospitals in The Netherlands. We award them a score of 3 on this criterion on par with Cambio.

Fit for purpose – clinical processes

Again we have to award Epic the highest score of 5. They have a large portfolio of clinical solutions.

Fit for purpose – PAS

As Epic doesn’t have any PAS functionality for the Danish market we have awarded them a score of 3 (Changed from 1 based on the comments from Epic).

Epic comment: Epic has the #1 PAS in the United States (as rated by KLAS) and we have also done PAS in The Netherlands. We reviewed your PAS list in the report and do most of it very well. Certainly we will need to do some development for the Danish market, but our PAS is very strong and may meet a high percentage of RH/RS needs already.

Fit for purpose – external integration

Epic has no installations in Denmark and thus there is no experience with how easily they can integrate to the existing external systems. We have no insight into the architecture of their technology and their data model that will allow us to judge their external integration capability. We have given all vendors without installations in Denmark the lowest score of 1 on this criterion.

Epic comment: Epic is an active participant in standards organizations such as HL7, and we work diligently to support new standards and versions to meet the needs of our clients and our applications.

Epic is ranked highest among major health IT vendors in the KLAS “Supports Integration Goals” category.

- Each year more than 13 billion data transactions happen between Epic systems and non-Epic systems. Over 8,900 interfaces help achieve this.

- Epic customers exchange patient data with systems from more than 350 vendors.

- Epic is the #1 EMR for e-prescribing, sending more prescriptions to pharmacies than any other vendor.

- 3.4 million clinical documents representing 760,000 patients are exchanged monthly by Care Everywhere – about 1/3 of the connections are to/from outside EHRs.

We offer a library of standard real-time interfaces that support an appropriate subset of features from HL7 versions 2.2 through 2.7, we support HL7 V3 XML implementable technical specifications, and we have released V3 interfaces. In addition to HL7 standards, we support the use of X12, DICOM, NCPDP, CCOW, COM, and many IHE interoperability profiles.

Software scalability – Current installation

Epic can point to several installations of the same magnitude as RH/RS. Large healthcare customers are their core market. They receive a 5 on this criterion.

Software scalability – SIG test

We have no information and have left this issue out of the comparison.

Software maintainability – SIG test

We have no information and have left this issue out of the comparison.

Price/Performance

We expect Epic to be the most expensive also when it comes to the price/performance ratio.

Winning the RH/RS projects would be nice for Epic, but not at any price. If price becomes a major issue they would probably be better off letting it go to one of the other vendors and move on to other projects, which are better paid.

Contrary to most of the other vendors Epic doesn’t need the RH/RS business. Epic has little incentive to come in low – it would hurt their position and reputation.

Implementation capability

We have not awarded high scores to any of the vendors when it comes to implementation capability. Staffing the projects with experienced and qualified local speaking staff will be a huge challenge for all vendors.

All vendors have teamed up with IT service organizations that have strong local representation. This is all very well, but none of them have any practical experience with the software and very few of them have staff with the required combination of clinical insight, process understanding and IT competencies.

Epic normally flies in a contingent of experts from their headquarters in Verona, Wisconsin to do the implementation. This certainly makes a lot of sense, but how non-Danish speaking staff will interoperate with the RH/RS staff and their NNIT colleagues is yet to be revealed.

We award EPIC a score of 2 on this criterion, which is the highest score we have assigned to any of the vendors.

Product strategy and influence

With Epic, RH/RS will be a small customer in a big shop. Epic will treat RH/RS exactly as they treat their other 285 customers. With Epic it will be “our way or the highway.”

We have given Epic the lowest score on this criterion.

Epic comment: We have a small number (285) of customers. If we’re selected, RH/RS would be near the top by size so RH/RS would not be a small customer in a big shop.

Political preference

Awarding a €135M IT healthcare project to a US supplier will be a hard one to swallow. It will silence the political rhetoric on which the Danish self-perception of being leaders in welfare technology is based. It will be giving Systematic – the Danish alternative – a very hard time.

Unless Epic makes an announcement promising to base an R&D center with 200 people in Copenhagen they will receive a low score on this criterion.

Staff Perks

Having Epic as a vendor will be a dream scenario for the decision makers and for the people involved in the project. Epic represents one of the largest IT healthcare platform communities in the world. With Epic you would never have to eat alone.

Epic gets the highest score on this criterion.

Cambio Healthcare Systems

Cambio is a Swedish company with 330 people exclusively focused on providing IT healthcare platforms. They are already in the Danish market with three installations: Region Syd, the Danish Army and the Faroe Islands. They have teamed up with Netcompany that has no reputation (thus also no bad reputation) in the healthcare industry.

Cambio is a Swedish company with 330 people exclusively focused on providing IT healthcare platforms. They are already in the Danish market with three installations: Region Syd, the Danish Army and the Faroe Islands. They have teamed up with Netcompany that has no reputation (thus also no bad reputation) in the healthcare industry.

References

Cambio was prequalified by being able to provide relevant life references. As opposed to the two Danish vendors, CSC- Scandihealth (who didn’t prequalify) and Systematic, Cambio has managed to win installations outside its home market.

Their headquarters are in Sweden. However, Cambio’s single largest installation is in Denmark.

We have awarded Cambio a score of 3 on this criterion (up from 2 based on the comments from Cambio).

Cambio comment: Our systems are also installed at over 30 hospitals in the UK.

Clinical reputation

With a 100% focus on IT healthcare platforms and activities in Denmark, Cambio is recognized as a serious player. Not on the same level as EPIC but a score of 4 is reasonable.

Cambio comment: Cambio is the only Nordic EHR (Electronic Health Records) vendor acknowledged by Gartner (ref. G00213874) alongside all other global EHR vendors.

HIMSS/EMRAM level 6/7

As with the other competitors, Cambio cannot show off a long list of HIMSS/EMRAM level 6/7 customers. However, Odense Universitetshospital has received a level 6 certification complementing the one client Cambio has in Sweden (Kronoberg). Thus, two out of three HIMMS level 6/7 institutions in the Nordics are Cambio customers.

We have given Cambio a score of 3 on this criterion.

Cambio comment: According to the European Commission the regionally integrated EHR and ePrescribing system in Kronoberg, Sweden, presents a benchmark from which many other European regions can learn a great deal. Source.

Fit for purpose – clinical processes

With 330 people focusing entirely on IT healthcare platforms and a nice Danish customer base we assume that the level of functionality is OK. Not at EPIC level, but enough to warrant a score of 4.

Fit for purpose – PAS

Cambio has three installations with PAS functionality for the Danish market. We have awarded a score of 5.

Fit for purpose – external integration

We have awarded Cambio and Systematic a score of 5 on the integration issue. They have installations in the Danish market and should understand and have demonstrated integration capabilities.

Software scalability – Current installation

Although Cambio claims several installations with 10,000 users or more, none of them are at the 10,000 concurrent users level. If the rate of concurrent to named users is 1:3 then there is a long way from 2,500 to 10,000 concurrent users.

We give Cambio a score of 2 on this criterion.

Cambio comment: We have several installations with 3,500 concurrent users.

Software scalability – SIG test

We have no information and have left this issue out of the comparison.

Software maintainability – SIG test

We have no information and have left this issue out of the comparison.

Price/Performance

If RH/RS tells Cambio to jump, Cambio will ask “how high?” Cambio could give away the software and still profit from the services and the value of the reference. Both Cambio and Netcompany will bend over backwards to get this deal.

We award Cambio a score of 5; not due to the performance aspect, but due their expected flexibility on price.

Implementation capability

Cambio can fly in in a contingent of Swedish speaking specialists and the jet lag will be less stressful than for Epic. However, a project the size of RH/RS will be a strain on Cambio.

We give them a 2 on this criterion.

Product strategy and influence

With Cambio, RH/RS will be a big customer in a medium-sized shop. RH/RS will receive special treatment, but they will not be the only customers in the neighborhood. They will become members of a Scandinavian user community and that may not be so bad.

We have given Cambio a 5 on this criterion.

Political preference

Awarding a €135M IT healthcare project to a Swedish supplier will support a minor adjustment in the political rhetoric. As Danes we can live well with the self-perception of being Scandinavian leaders in welfare technology. If we choose a Swedish solution now, then they owe us one.

It is not the perfect political option but it is worth a score of 4.

Staff Perks

Cambio will not be a personal favorite among the decision makers. Field trips to Northern Sweden don’t have the same attractiveness as Verona, Wisconsin.

Cambio gets a 2 on this Criterion.

Cerner is also one of the giants in providing IT healthcare platforms. Annual turnover is over $2B and they are very profitable. They have a staff of close 12,000 “associates” (the Cerner name for an employee) in 23 offices around the globe. Approximately 7.800 “associates” are based in Kansas City, home of Cerner’s World Headquarters. 700 associates in Europe are working on implementing systems in the UK, France, Germany, Spain, Ireland, Austria.

Cerner is also one of the giants in providing IT healthcare platforms. Annual turnover is over $2B and they are very profitable. They have a staff of close 12,000 “associates” (the Cerner name for an employee) in 23 offices around the globe. Approximately 7.800 “associates” are based in Kansas City, home of Cerner’s World Headquarters. 700 associates in Europe are working on implementing systems in the UK, France, Germany, Spain, Ireland, Austria.

Cerner has teamed up with CGI, previously Logica, who was with Cambio on Region Syd (adultery in the IT business is not unusual!).

References

Cerner is in the same league as Epic as far as references are concerned. Cerner have a much broader international presence than Epic as more than 400 of their 1,100 installations are outside the US.

A clear 5.

Clinical reputation

The clinical reputation of Cerner is unquestionable, however they do not have a big presence in the Scandinavian market. Apparently they have an installation in Sweden, but not the IT healthcare platform domain. A search for “Sweden” on their corporate web site gives no results.

We award them a score of 3+

Cerner comment: Regarding installation in Sweden, we have a PACS archive client in Sweden.

HIMSS/EMRAM level 6/7

Cerner has one level 7 HIMSS/EMRAM client in Spain (Hospital de Dénia, Valencia) and ten level 6 HIMSS/EMRAM clients in France, Malaysia, United Arabic Emirates, Saudi Arabia, Chile and Canada. In the USA, Cerner has 32 clients with level 7 HIMSS/EMRAM and 142 clients with HIMSS/EMRAM level 6.

We award them a score of 5 (changed from 3 based on the comments from Cerner)

Fit for purpose – clinical processes

Cerner will be able to deliver most of the functionality required. A clear 5.

Fit for purpose – PAS

As Cerner doesn’t have any PAS functionality for the Danish market we have awarded a score of 3. (Changed from 1 based on the comments from Cerner)

Cerner comment: PAS has been delivered in the Australia, UK, Spain and France, so a proof that we have been able to deliver outside of the US and adapt to local requirements and national system interfaces.

Fit for purpose – external integration

As Cerner is not present in the Danish market they automatically get a 1.

Software scalability – Current installation

Cerner has many references much larger than RH/RS. A clear 5.

Software scalability – SIG test

We have no information and have left this issue out of the comparison.

Software maintainability – SIG test

We have no information and have left this issue out of the comparison.

Price/Performance

We can only repeat the consideration made about Epic. RS/RH is a “nice to have” customer for Cerner, but they are hardly going to change their communication to NASDAQ if they are not awarded the deal.

Cerner will be strong on performance, but very inflexible on price. Probably a little more commercially oriented than Epic so we give them a score of 2.

Implementation capability

Cerner has teamed up with CGI. CGI may have some domain competencies from their work with Cambio in Region Syd. On CGI’s (Logica’s) Danish web site they still promote Cambio, but don’t mention anything about Cerner.

We assume that if Cambio should win the business CGI’s will still pick up the phone should they receive a call from RH/RS.

We give Cerner a 1.

Product strategy and influence

Cerner is an international player with a very large footprint outside the USA. We believe the same considerations as we gave Epic will apply for Cerner.

We have given Cerner a 1 on this criterion.

Political preference

Repeating the considerations for Epic: Awarding a €135M IT healthcare project to a US supplier will be a hard one to swallow. It will silence the political rhetoric on which the Danish self-perception of being leaders in welfare technology is based. It will be giving Systematic – the Danish alternative – a very tough time.

Unless Cerner makes an announcement promising to base an R&D center with 200 people in Copenhagen, Cerner will receive a low score on this criterion.

We award them a score of 2.

Staff Perks

Cerner definitely represents a global community, but they don’t have the same esteem as Epic.

We award Cerner a score of 4.

![]() Siemens, with headquarters in Munich, is one of the largest European suppliers of IT healthcare platforms. Their representation in the US market came with the acquisition of Shared Medical Systems in 2000. In 2009 Siemens acquired “i.s.h.med” software from T-Systems in Austria adding another 300 hospitals to the customer base of approximately 1,200 hospitals. The i.s.h.med system is fully integrated with the SAP healthcare software.

Siemens, with headquarters in Munich, is one of the largest European suppliers of IT healthcare platforms. Their representation in the US market came with the acquisition of Shared Medical Systems in 2000. In 2009 Siemens acquired “i.s.h.med” software from T-Systems in Austria adding another 300 hospitals to the customer base of approximately 1,200 hospitals. The i.s.h.med system is fully integrated with the SAP healthcare software.

We assume that Siemens will be offering the Soarian MedSuite platform to RH/RS.

Siemens has teamed up with KMD and ATOS.

KMD was recently acquired by American Advent International and has Léo Apotheker as the new chairman of the board. KMD (previously Kommune Data) was the de facto monopolist in the Danish PAS market (Patient Administrative Systems) in the ’70’s and ’80’s, but sold the business unit to CSC Scandihealth. KMD is now attempting a come back through the alliance with Siemens.

ATOS acquired Siemens IT Solutions and Services in July 2011 making them one of the largest providers of Managed Services and Systems Integration in the IT industry.

References

Siemens has over 50 references with the Soarian MedSuite platform in Europe alone. Not in the league of Cerner and Epic but enough to score a 4.

Clinical reputation

Siemens certainly has a solid reputation in the clinical domain but it is not a consistent reputation. The many various solutions and platforms have made Siemens a recognized brand, but the brand values are not always clear.

We have awarded Siemens a 3+ score for clinical reputation.

HIMSS/EMRAM level 6/7

Siemens has one HIMSS/EMRAM level 7 installation. The Universitätsklinikum Hamburg-Eppendorf was awarded level 7 certification in October 2011.

We award Siemens a score of 2 on this criterion.

Fit for purpose – clinical processes

Siemens are investing heavily in IT healthcare platforms. With a solid position in the German market there is no reason to believe that they do not have very deep functionality across most clinical areas.

We award Siemens the highest score of 5 on this criterion.

Fit for purpose – PAS

As Siemens doesn’t have any PAS functionality for the Danish market we have awarded a score of 1.

Fit for purpose – external integration

As Siemens is not present in the Danish market they automatically get a 1.

Software scalability – Current installation

Siemens has many references much larger than RH/RS. A clear 5.

Software scalability – SIG test

We have no information and have left this issue out of the comparison.

Software maintainability – SIG test

We have no information and have left this issue out of the comparison.

Price/Performance

With three companies headed by a giant like Siemens we don’t see much flexibility in pricing. We believe a score of 2 is reflecting the willingness to adjust the pricing.

Implementation capability

All vendors have made strategic alliances out of necessity. An alliance with three parties is less attractive than an alliance with two parties. The preferred supplier is one that has the full control and doesn’t need a strategic alliance at all.

We consider the tripartite constellation with KMD and ATOS a weakness and award Siemens a score of 1 for implementation capability.

Product strategy and influence

None of the three companies in the Siemens alliance will suffer from losing this deal. We don’t see RH/RS getting a major say on the direction of the Siemens healthcare roadmap. We believe Siemens will listen a little more than Epic and Cerner and award them a score of 2.

Political preference

Awarding a €135M IT healthcare project to a German supplier will require a major adjustment in the political rhetoric. As Danes we will have a hard time adopting a self-perception of being among European leaders in welfare technology. It just doesn’t have the right ring to it.

Making a choice for a German supplier is better than choosing a US supplier. We give Siemens a score of 3 on the political preference.

Staff Perks

Although Siemens is a dominating player in the market for IT healthcare platforms we don’t believe they have the same standing as Epic and Cerner.

The personal benefits will be higher than Cambio and Systematic so we award Siemens a score of 3

![]() Exactly what made Systematic choose to let IBM lead the tender is unclear. Probably the expectation that RH/RS would appreciate the deep pockets of IBM and thus minimize the risk associated with Systematic’s financial capabilities associated with a €135M deal.

Exactly what made Systematic choose to let IBM lead the tender is unclear. Probably the expectation that RH/RS would appreciate the deep pockets of IBM and thus minimize the risk associated with Systematic’s financial capabilities associated with a €135M deal.

We will assume that IBM will propose Systematics Columna platform and that IBM will deliver auxiliary services.

Systematics is primarily a software engineering company. The company employs 450 people, which is quite large in a Danish context. However Systematic have spread their activities over four verticals and are operating in Denmark, the UK, the USA, Australia, Germany, Finland and Sweden.

We estimate that Systematic has around 100 people working on their healthcare solutions.

Systematic is in tough company and the CEO has already submitted the first S.O.S. stating that if they don’t win this project, international market expansion will be very difficult.

References

Systematic has one installation. “Region Midt” in Denmark. They receive a score of 1.

Clinical reputation

We have awarded Systematic a score of 3 for clinical reputation. Compared to the other vendors this may be far too high, but they do have a position in the Danish market with one customer.

HIMSS/EMRAM level 6/7

Systematic cannot show a HIMSS/EMRAM level 6 or 7 installation. They receive a score of 1.

Fit for purpose – clinical processes

With just one installation and as relatively new in this industry, we assess that Systematic still have a way to go meeting the level of clinical functionality available from the more established vendors. We award them a score of 3

Fit for purpose – PAS

Systematic has one installation with PAS functionality for the Danish market and so we have awarded the highest score of 5.

Fit for purpose – external integration

As Systematic already has an installation in the Danish market, we automatically award them the highest score of 5.

Software scalability – Current installation

Systematic cannot show any healthcare installations of the same magnitude as RH/RS. We award them a score of 1.

Software scalability – SIG test

We have no information and have left this issue out of the comparison.

Software maintainability – SIG test

We have no information and have left this issue out of the comparison.

Price/Performance

What Systematic will lack in functionality and references they will compensate with flexibility on pricing. As they have chosen IBM as the bid leader they may not have the final word on this issue. Nevertheless, we have awarded them the highest score of 5.

Implementation capability

As Systematic is has its headquarters in the Danish market, we have awarded them the highest score of 2 in this category.

Product strategy and influence

Winning this deal is extremely important for Systematic. Losing 50% of your domestic market to a foreign competitor is like the kiss of death. In a customer relationship with RH/RS, Systematic will be very responsive.

We award Systematic a score the highest score of 5 on this criterion.

Political preference

Awarding a €135M IT healthcare project to a Danish supplier based on fair competitive conditions will be a major national achievement. Danes are proud people and we see no reason for not claiming world superiority in many professional disciplines. Winning this project will sustain the self-perception that we are world leaders in welfare technology.

Unfortunately this agenda needs to be operated well under the radar. Danish industry will have much to lose if other nations also favor their national suppliers. The EU legislation will make the doors wide open for vendor complaints if there is just the slightest suspicion of political pressure.

We award Systematic a score of 5 for political preference, but they have to play their cards very carefully as the rhetoric may turn against them.

Staff Perks

We believe that the stakeholders’ personal preferences will not support a selection of Systematic. The company unfortunately represents one of the smallest IT healthcare communities in the world.

We award Systematic a score of 2 on the same level as Cambio.

[/wpspoiler]

In the following section you will find more information on the justification of and the current significance we have assigned to each criterion. On March 11, 2013 the vendors will submit their first proposals. As we approach the end of April 2013, RH/RS will select the three vendors for the final selection. With these three vendors RH/RS will dig deeper and final proposals should be submitted by the end of June 2013. The rest of 2013 will be used for final vendor selection and contract negotiations.

[wpspoiler name=”Selection Criteria Details and Priorities”]

Installed base and references

It has been clear from the very beginning of the procurement process that RH/RS didn’t want to play the role of guinea pigs. They wanted technology that was already developed, technology that was in production elsewhere in the world and could be demonstrated in real life situations.

The prequalification process where the eight applying vendors were reduced to five was exclusively based on reviewing references. The “installed base and reference” criteria excluded the current supplier and Danish market leader CSC Scandihealth from the process.

The “installed base and reference” criteria will not play a major role in the selection of the three vendors for the final qualification and selection process, but it may resurface later on. Read more about this later in this article where we elaborate on the “Political Power Play”.

We have estimated the current weight of the reference criterion to 5%.

Clinical Reputation

The demand side of the healthcare industry is global.

The demand side – doctors, nurses and administrators – travel the world participating in conventions, congresses, site visits etc. They know what is available and they have a very global mindset.

The demand side wants a supplier that is a recognized player in the global and the local market. “They” prefer someone they already know and trust.

The “Clinical Reputation” criterion may not be on the official list of selection criteria, but it is in the sub-consciousness of each of the decision makers and influencers.

At this stage the criterion doesn’t play a major role role, but as we get closer to the reduction from 5 to 3 vendors it will play an increasingly important role. We believe Systematic and Cambio will suffer most from the change in the importance of this criterion as they represents the smallest healthcare communities among the five long-listed vendors.

We have estimated the current weight of the clinical reutation criterion to 5%.

HIMSS/EMRAM level 6/7 certifications

Despite the political rhetoric surrounding the superiority of Danish welfare technology we are hopelessly behind in providing IT support for the secondary healthcare sector (the hospitals). It is the US that are leading the implementation of IT healthcare platforms that drive the productivity of the healthcare worker, the empowerment of and the service available to the patients and the reporting and data mining facilities available to the financial “sponsors.”

The level of “paperless and transparent” production in healthcare institutions is measured and certified according to the HIMSS/EMRAM (Electronic Medical Record Adoption Model) definitions. RH/RS is currently at level 3. The RH/RS ambition is to make it to level 6 with the current project and to level 7 (the top level) within the next few years. Level 7 certification requires an IT platform that can support the paperless production infrastructure.

RH/RS will pay serious attention to which solutions are already supporting HIMSS/EMRAM level 6 and 7 certified institutions.

The number of current level 6 and 7 certifications will be a selection criterion with increasing importance and probably already decisive for the selection of the vendors for the short list of three.

We have estimated the current weight of the HIMSS/EMRAM level 6 and 7 criterion to 5%.

Fit for purpose

RS/RH has spent considerable time and effort defining a demanding yet realistic set of functional requirements. Through site visits prior to the tender process and dialog meetings with the five prequalified vendors, RH/RS has an up-to-date overview of the functionality currently available, what is in the R&D pipelines and what remain as good intentions in the product development roadmaps.

The degree of fit between the functional requirements and the vendors’ capability of demonstrating availability or at least prototypes in the pipeline is currently the most important set of criteria.

Fit for Purpose – clinical functionality

“Doctors are difficult” is a standard statement in the healthcare industry. No doubt that clinical healthcare workers are demanding, well educated and outspoken, but they also work in a “mission critical” and highly complex environment.

The match between the clinical requirement specifications and what the vendors can demonstrate being available will be one of the most deciding criteria.

The three vendors making it to the final round will have to demonstrate their solutions for 500 clinical and administrative users. Unified and unambiguous feedback from these users will be impossible to ignore. Finally the software will be installed in the ITX lab at Herlev hospital and simulation tests will be performed.

For now, we have estimated the fit for clinical purpose criterion a 25% importance.

Fit for Purpose – PAS

The Patient Administrative System elements cover areas such as:

- Admission

- Master Patient Index

- Appointment Booking

- Waiting List Management

- Record of Patient Activity

- Activity Billing

- Reporting

While pneumonia, appendicitis and fractures are the same all over the world and thus in principle can be clinically managed the same way, PAS is very different from country to country. It is exactly the differences in PAS processes and requirements that make it so difficult for IT healthcare platforms to travel across borders.

Systematic and Cambio has PAS functionality for the Danish market and thus enjoy a considerable advantage over the foreign vendors.

All the foreign vendors will be able to develop Danish PAS functionality, but with the ambitious rollout schedule RH/RS has defined any software development activity will represent a major risk. The foreign vendors will also suffer from the fact the cost of PAS development for Denmark cannot be shared with more customers. PAS functionality for Denmark is not passing the threshold to a huge market like Great Britain, Germany, France, Italy or Spain.

We have assigned a 15% priority to the “Fit for purpose – PAS” criterion. As we get closer to the final decision this criterion may gain priority.

Fit for purpose – external integration

Any IT healthcare platform will have to receive data from and deliver data to external systems. Some of the clinical functionality, which is not a part of the vendor’s core application, may be made available through integration with a third party subsystem.

An IT healthcare platform’s ability to integrate to external systems is critical for the smooth operation of a healthcare institution. We have assigned a 15% importance to this issue.

Software scalability – current installations

RH/RS has approximate 40,000 IT users of which 10-12,000 will be on the system at any point in time (concurrent users).

The time it takes from a user hitting a button to the system responding shouldn’t be more than one second. Increasing response times have a very negative impact on user productivity way beyond the response time itself.

All large IT installations suffer from performance issues and keeping up performance is an ongoing activity.

RH/RS are extremely alert to this issue and are verifying that the vendors have live installation with at least the same amount of users and transactions. Scaling a system from 1,000 concurrent users to 12,000 concurrent users is not trivial. RH/RS will ask for verification from the smaller vendors that scaling is possible (and economically feasible).

The ability to demonstrate scalability will not be so critical if the SIG test comes out favorably for a vendor.

Software scalability – SIG test

To assess the quality of the software in terms of scalability RH/RS has contracted with the Software Improvement Group (SIG).

The vendors have uploaded their source code to RH/RS and SIG has performed analysis on the scalability of the code.

The result of the findings may disqualify those vendors showing severe issues in software scalability. Scalability is a knockout criterion.

Software maintainability – SIG test

Software is buggy and must be fixed from time to time. Software is extendable and new releases with new features will be made available.

The maintainability and extendibility of the software is an important element of the daily operation of the IT healthcare platform.

SIG has also been asked to assess the vendor’s code in terms of maintainability and extendibility.

We are uncertain how much importance this issue will receive.

Price/Performance

“Price is always an issue” is the normal saying.

In this situation both the price and the performance will be highly composite entities. RH/RS will do an honest effort of making the proposals comparable. However, making the proposals 100% comparable is simply not possible. There will be plenty of room for pushing all sorts of interests into the mix.

Most of the stakeholders in the decision making process are not concerned with the price. This is a common trait in decision making in large organizations: “It is somebody else’s money”. Thus there will probably be an upper threshold, but not any premium for coming in low.

Implementation capability

A very big portion of the €135M will be used for project management, training customization, integration etc. All service quality depends on the experience and competencies of individual people, the management frameworks applied and the leadership demonstrated. The vendors will have to make quality people available in high volumes to perform the rapid roll-out.

This is with no exception a genuine challenge for all vendors.

We have assigned a 10% weight on the criterion. It may grow to over 50% as we get closer to the final decision.

Product strategy and influence

Do we have a Scandinavian healthcare model? Do we have Scandinavian healthcare processes? Do we want to remain in the driver’s seat as far as the development of healthcare standards in Scandinavia are concerned? If so, then we should choose a vendor that will listen to us and maintain his R&D roadmap together with us.

Do we want to adapt to world standards and follow best practices defined in the major countries? Then we should choose one of the global players and follow their roadmap.

Do we want to be a big and important customer or do we prefer to be a small and less significant customer?

These questions and options are important for RS/RH, the Danish healthcare system and the nation.

We assume that RS/RH, the Danish healthcare system and the nation will prefer to have substantial influence on the R&D roadmap of the chosen supplier. If so, Systematic and Cambio will benefit.

If we are wrong EPIC, Cerner and Siemens will benefit.

Political preference

History has proven that it has been very difficult for IT healthcare platform providers to achieve international growth. Neither Systematic nor CSC Scandihealth has achieved any international traction with their [slider title=”EHR”] Electronic Health Record [/slider] systems.

Why?

Because each country has had their national (at times protectionist) agenda and their local vendors. The barriers to entry have been enormous. Existing personal relationships, lack of local representation, differences in clinical as well as patient administrative procedures have been keeping foreign vendors out.

All this is changing.

Clinical procedures are getting more and more standardized. Over the last 10 years, the US based vendors especially have developed systems that can be used within multiple customer infrastructures. These justify independent (not customer specific) R&D plans and activities. The Danish [slider title=”market”] a market with just 5 potential customers is hardly a market [/slider] has been far too small to support an IT healthcare platform industry of the two local vendors (CSC Scandihealth and Systematic).

The IT healthcare platform industry is maturing and is gradually becoming a product industry rather than a bespoke software engineering industry.

While RH/RS may not suffer from any political bias, the Danish parliament and the central administration may have a hard time matching the rhetoric around superior Danish welfare technology with the choice of a US vendor for the support of healthcare for half of its’ population.

We are convinced that a lot of people hope and pray that Systematic fares well in the technical evaluations. Because if they don’t we can wave goodbye to a Danish IT healthcare platform industry and note a torpedo in the waterline of the rhetoric around the superior Danish welfare technology.

Political preference is not an official decision criterion, but read the newspapers and you can observe that the political lobby is already on full speed.

We have only assigned a small weight to the political criterion. However, when we get closer to the final decision and the decision makers start to disagree internally, then the political criterion will gain power.

Staff perks and community participation

Staff perks is not on the official list of decision criteria either. When people are involved in large procurements of a strategic nature, they obviously also consider what serves their own individual interests.

Is it more “fun” to have a supplier in the USA than one in Aarhus? Will experience with Epic or Cerner make you more valuable than experience with Systematic/Columna? Are you better off being a part of the Siemens user community than being part of the Cambio Cosmic user community?

No one will reveal their individual preferences, but they will be there and they will influence how each decision makers prioritize and evaluate the other decision-making criteria.

Disclaimer

This article is primarily based on publicly available information, comments from the vendors and the interpretation and evaluation of TBK Consult. Corrections of factual information as well as challenges to our assessments are welcomed. All the statements and assessments expressed in this article are proprietary of TBK Consult. TBK Consult is not affiliated with RH/RS and RH/RS has not been asked to comment this article nor have they done so.

Related Articles

- Danish Healthcare Mega Investment Requires a Pragmatic Approach to Selecting New Software

- Danish healthcare’s mega IT investment vendor qualification is based on Software Quality Assessment

- How Danish healthcare authorities should structure their final software RFP

- Withdraw or lose? – The challenge for 4 of the 5 vendors in Danish EMR mega project

- Breaking News: IBM, Epic and Cerner to compete for Danish €135M healthcare IT project

- Why the €135M Healthcare Platform Project Went to Epic/NNIT